A July 4 email from the Social Security Administration claimed that Congress had eliminated federal income taxes on Social Security benefits, when it had not

This post has been republished from Professor Patricia McCoy’s Substack. Her new book, “Sharing Risk: The Path to Economic Well-Being for All,” is available from The University of California Press.

During last year’s presidential race, President Trump declared: “Seniors should not pay taxes on Social Security and they won’t,” according to CBS News. This promise to end income taxes on Social Security benefits was the single most popular economic proposal of either candidate, according to an ABC News/Ipsos Poll conducted about a month before the election. In fact, voters were so enthralled with his idea that 85% of people polled approved.

Yet H.R. 1, the budget reconciliation bill signed into law this July 4, did not eliminate income taxes on Social Security payments. That did not stop Social Security from claiming otherwise after H.R. 1 became law.

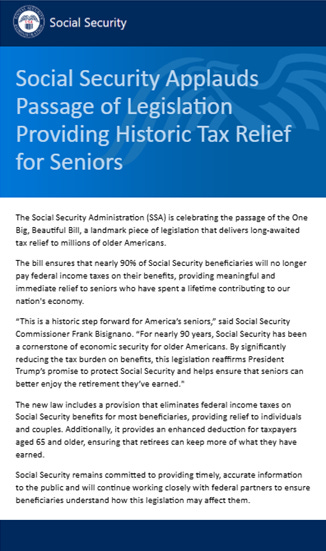

On July 4, I received this curious email from the Social Security Administration:

Strikingly, the Social Security Administration claimed that the “new law includes a provision that eliminates federal income taxes on Social Security benefits for most beneficiaries, providing relief to individuals and couples.” The email went on to say, “Additionally, it provides an enhanced deduction for taxpayers aged 65 and older,” which suggested that there was a separate provision eliminating income taxes on Social Security on top of that deduction. But H.R. 1 did not eliminate income taxes on Social Security. So what gives?

First: How Income Taxes on Social Security Work

To get a handle on that mysterious Social Security Administration email, first it’s worth a short tour of how income taxes on Social Security benefits work. The big takeaway is this: almost two-thirds (64%) of Social Security recipients age 65 and up don’t owe income taxes on their benefits. Those who do are higher income. Yet many people mistakenly assume they will owe income tax on their Social Security benefits when in fact they will not, judging from the astonishing popularity of President Trump’s proposal.

Under federal tax law, people don’t have to pay income tax on their Social Security benefits unless their incomes are high enough. To figure that out, take half your Social Security benefits and add your “modified adjusted gross income” (i.e., your other income after the IRS makes certain adjustments). If the total exceeds $25,000 ($32,000 for a couple filing jointly), you will owe federal income taxes on some portion of your Social Security income. And if that total exceeds $34,000 (or $44,000 for joint returns), an even higher portion of your Social Security income will be taxed.

As we saw, a majority pays no income taxes on Social Security at all. For those who do, their tax liability is often small. In this subset of recipients who do pay taxes, those earning under $63,300 pay an average of 1% or less of their Social Security benefits in income taxes. Compare that to the top 20% of Social Security beneficiaries (with incomes over $205,800), who pay 20% of their Social Security benefits on average in income taxes. Thus, cushy retirees pay the most income taxes on Social Security payments and have the most to gain from reductions in those taxes.

What Congress Did Do in H.R. 1

The Administration was just plain wrong: Congress did not repeal income taxes on Social Security benefits in H.R. 1. It did not even amend the formula that I just described for calculating those taxes.

But Congress did enact a different provision that will indirectly reduce the number of people age 65 and older who owe income taxes on their Social Security benefits. And for some people who still owe those taxes, the amount owed will be reduced.

So, what are the specifics? In H.R. 1, Congress created a new $6,000 deduction for taxpayers who are age 65 or above ($12,000 for married seniors). This so-called “enhanced deduction” is stacked on top of the existing $15,750 standard deduction ($31,500 for married couples) and the extra $2,000 standard deduction for single taxpayers age 65 and over ($3,200 for married seniors filing jointly). The enhanced deduction also applies to taxpayers who itemize deductions.

The enhanced deduction comes with strings attached, however. First, the new tax break for older adults only lasts four years and will expire on December 31, 2028. That’s just weeks after the next presidential election. Go figure.

Second, the full $6,000 (or $12,000) amount does not apply to everyone age 65 and up. It only goes to taxpayers who have modified adjusted gross incomes of $75,000 or less (or $150,000 or less for a joint return). Above that, the amount of the deduction drops on a sliding scale by income, until it reaches $0 for taxpayers with modified adjusted gross incomes over $175,000 (or $250,000 for joint returns).

Third, the deduction does not apply to Social Security recipients (or anyone else) under age 65. Some of these people receive old age benefits, while others receive Social Security disability or survivors’ benefits. Notably, the White House was silent about leaving these groups in the dust when it crowed “No Tax on Social Security” shortly before the enactment of the bill.

How the New Enhanced Deduction Will Affect Who Owes Income Taxes on Social Security

Depending on the person, the new enhanced deduction will free more senior citizens from owing any federal income taxes on their Social Security benefits. According to the Council of Economic Advisers, 88% of all seniors age 65 and higher receiving Social Security will pay no income tax on those benefits under this provision. That is up from 64% presently.

For some senior citizens who still do owe federal income taxes on Social Security, the new deduction will reduce their taxable income and with it, the amount of federal income tax they will owe on those benefits. These retirees are upper-middle income or higher (although the wealthiest seniors will get no tax cut at all under the enhanced deduction).

Smoke and Mirrors in Washington

So why did the Social Security Administration falsely suggest that Congress had repealed income taxes on Social Security benefits outright? Apparently, it wanted to give the appearance that the Trump campaign had delivered on its promise to rescind those taxes. But H.R. 1 did nothing of the sort. In fact, around 20 million recipients will still have to pay Uncle Sam taxes on their Social Security benefits under the new law: 13 million recipients under age 65 and 7 million higher-income recipients age 65 and up.

That’s not the only way the Social Security email sold people a bill of goods. In addition, it pretended that H.R. 1 actually benefited every Social Security recipient age 65 and higher. But even before that law was passed, almost two-thirds of seniors age 65 and up were not paying income taxes on Social Security because they earned too little. Instead, the only ones who got relief from income taxes on Social Security in H.R. 1 were upper-middle and higher-income seniors.

Given who really benefits from the enhanced deduction, isn’t it interesting how the 2024 Republican presidential campaign whipped up a frenzy of popular support for repealing income taxes on Social Security? That campaign pledge exploited people’s mistaken belief that they would owe those taxes starting at age 65, when virtually two-thirds of them would not. For that two-thirds share of voters, the campaign pledge was just an empty promise.

Coda

Let me conclude with three reasons why we should care about the misleading nature of the Social Security Administration’s email.

First, that email could deceive some Social Security recipients into thinking that they will not have to file federal tax returns, when in fact they will. That mistake could have serious enforcement consequences for those individuals.

Second, the enhanced deduction will further impair Social Security’s solvency. The Social Security Old-Age and Survivors Insurance Trust Fund is slated to go broke in 2033, as I discuss in my new book, Sharing Risk: The Path to Economic Well-Being for All. And that forecast was before the passage of H.R. 1.

H.R. 1 will hasten the Trust Fund’s demise by reducing one of its funding sources. Currently, federal income taxes on Social Security benefits make up about 4% of the Trust Fund’s revenues. By the Joint Committee on Taxation’s latest estimate, the enhanced deduction will cost $93 billion in lost tax revenues for the four years it is in effect. We can disagree on how big an effect that will be, but one thing’s for certain: the enhanced deduction will only make Social Security’s insolvency worse, to the detriment of beneficiaries.

Finally, and of top concern, the Social Security Administration’s email eroded the public’s faith in the trustworthiness of the Social Security system by distorting the truth. It is vital for the Social Security Administration to be non-partisan and honest because the entire country depends on it for people’s economic security. People should be able to rely on the Social Security Administration for the unvarnished truth in all matters affecting their benefits. Instead, the agency’s misbegotten email stands to reinforce voters’ cynicism that the system is rigged against retirees of modest means in favor of their better-off counterparts.

This post has been republished from Professor Patricia McCoy’s Substack. Her new book, “Sharing Risk: The Path to Economic Well-Being for All,” is available from The University of California Press.